The Federal Reserve's $16 Trillion Back-door Bailout

The financial coup d'etat: bankers are demanding (and getting) governments to rebuild their loan reserves at labor's expense, thereby making ordinary people bear the burden of 'bailing out' the economic elite. Working households, of course, are the most affected, with spending cuts and high unemployment taking a punishing toll. More austerity is coming under the guise of reducing the federal debt, assuring greater deprivation. The worst is yet to come. - Stephen Lendman, Destructive Neoliberal Austerity, thepeoplesvoice.org, November 23, 2010Derivatives: The Real Reason Bernanke Funnels Trillions Into Wall Street Banks

Seeking AlphaFebruary 8, 2011

We’ve been over the numerous BS excuses that US Dollar destroyer extraordinaire Ben Bernanke has made for QE enough times that today I’d rather simply focus on the REAL reason he continues to funnel TRILLIONS of Dollars into the Wall Street Banks.

I’ve written this analysis before. But given the enormity of what it entails, it’s worth repeating. The following paragraphs are the REAL reason Bernanke does what he does no matter what any other media outlet, book, investment expert, or guru tell you.

Bernanke is printing money and funneling it into the Wall Street banks for one reason and one reason only. That reason is: DERIVATIVES.

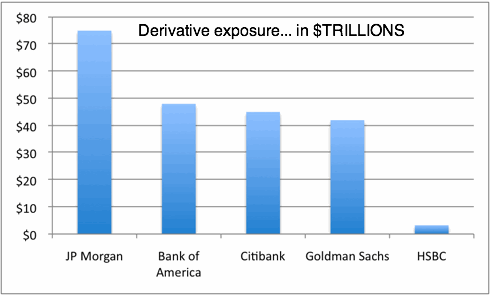

According to the Office of the Comptroller of the Currency’s Quarterly Report on Bank Trading and Derivatives Activities for the Second Quarter 2010 (most recent), the notional value of derivatives held by U.S. commercial banks is around $223.4 TRILLION.

Five banks account for 95% of this. Can you guess which five?

Looks a lot like a list of the banks that Ben Bernanke has focused on bailing out/ backstopping/ funneling cash since the Financial Crisis began, doesn’t it? When you consider the insane level of risk exposure here, you can see why the TRILLIONS he’s funneled into these institutions has failed to bring them even to pre-Lehman bankruptcy levels.

Ben Bernanke is a stooge and a fraud, but he is at least partially honest in his explanations of why he wants to keep printing money. The reason is to try to keep interest rates low. Granted, he’s failing miserably at this, but at least he understands the goal.

Of course, Bernanke tells the public and Congress that the reason we need low interest rates is to support housing prices. He doesn’t mention that $188 TRILLION of the $223 TRILLION in notional value of derivatives sitting on the Big Banks’ balance sheets is related to interest rates.

Yes, $188 TRILLION. That’s thirteen times the US’ entire GDP, and nearly four times WORLD GDP.

Now, of course, not ALL of this money is “at risk,” since the same derivatives can be traded/spread out dozens of ways by different banks as a means of dispersing risk.

However, given the amount of money at stake, if even 4% of this money is “at risk” and 10% of that 4% goes wrong, you’ve wiped out ALL of the equity at the top five banks.

Put another way, Bank of America (BAC), JP Morgan (JPM), Goldman (GS), and Citibank (C) would CEASE to exist.

If you think that I’m making this up or that Bernanke doesn’t know about this, consider that his predecessor, Alan Greenspan, knew as early as 1999 that the derivative market, if forced into the open and through a public clearing house, would “implode” the market. This is DOCUMENTED. And you better believe Greenspan told Bernanke this.

In this light, all of Bernanke’s monetary policies and efforts are focused on doing one thing and one thing only: trying to shore up the overleveraged, derivative-riddled balance sheets of the Too Big to Fails, or Too Bloated to Exist, as I like to call them.

The fact that the bank executives taking this money and using it to pay themselves and their employees record bonuses only confirms that these folks have NO interest in taking care of shareholders or their businesses. They’re just going to take the money and run for as long as this scheme works.

I don’t know when this will come unraveled. But it WILL. At some point the $600+ TRILLION behemoth that is the derivatives market will implode again. When it does, no amount of money printing will save the Too Bloated To Exist banks’ balance sheets.

At that point, it’s game over for Wall Street and the Fed.

So there we have President Obama expressing guarded support for the Egyptian people in their uprising against those corrupt, entrenched interests, while at home, he’s unable to do terribly much about interests like JP Morgan Chase. For one thing, they’ve got the government pretty well sewn up. Not bad to have an executive from your bank (Bill Daley) recently appointed as the president’s Chief of Staff, and to have your bank’s CEO (Jamie Dimon) on particularly friendly terms with the Treasury Secretary. It’s not just Chase. Along with Deutsche Bank, UBS was yet another bank having known about and done nothing about Bernie Madoff. That bank is so close with Obama it goes on vacation with him. If we’re going to stop being hypocrites, we have to apply the same standards to rotten institutions wherever they are. - Russ Baker, Giving Chase: Egypt, OK – But What About America’s Oligarchs?, LewRockwell.com, February 14, 2011

The Feds $16 Trillion Back-door Bailout - the Biggest Scam in World History

Dr. Mercola

February 9, 2011

The greatest scam in history has been exposed -- and has largely been ignored by the media. In fact, it’s still going on.

The specifics of a secret taxpayer funded “backdoor bailout” organized by unelected bankers have been revealed. The data release revealed “emergency lending programs” that doled out $12.3 trillion in taxpayer money ($16 trillion according to Dr. Ron Paul) -- and Congress didn’t know any of the details.

According to the Public Record:

Sources:“The Federal Reserve was secretly throwing around our money in unprecedented fashion, and it wasn’t just to the usual suspects like Goldman Sachs, JP Morgan, Citigroup, Bank of America, etc.; it was to the entire Global Banking Cartel.

To central banks throughout the world: Australia, Denmark, Japan, Mexico, Norway, South Korea, Sweden, Switzerland, England ...

We are talking about trillions of dollars secretly pumped into global banks, handpicked by a small select group of bankers themselves. All for the benefit of those bankers, and at the expense of everyone else.”

The Public Record December 10, 2010

Video Transcript

Dr. Mercola's Comments:

I recently had the pleasure of interviewing Congressman (TX) Dr. Ron Paul about these secret "backdoor bailouts" that amount to a staggering $16 trillion. (To get a better idea of just how much money this is, see What Does a Trillion Dollars Look Like?)

An AMAZING fact: The Federal bailout is more than the cost of the First World War, the Second World War, the Korean War, the Vietnam War, Marshall Plan, the New Deal, the Invasion of Iraq, and landing on the moon COMBINED!

And, with this bailout Obama has nearly created more debt than ALL the previous presidents COMBINED.

Dr. Paul is now the Chairman of the Congressional subcommittee overseeing the Federal Reserve, which as you may know, is a private entity yet largely responsible for our economic policies.

The Federal Reserve has now handed out multi-trillion dollar bailout packages to banks and big industries, and now, finally, people are starting to demand to know where all that money actually went—which is largely how Dr. Paul came to be the Chairman of this subcommittee in the first place.

To get answers, Dr. Paul, along with his son, has introduced legislation to enable an audit of the Federal Reserve. When asked what he thinks the audit might reveal, he says:

"The reason to have an audit is to find out what they're hiding. The information they're most protective of are the details of where many trillions of dollars used in the bailout went, and what the collateral was."

The Federal Reserve has also been extremely protective of information dealing with foreign central banks. However, according to Dr. Paul, preliminary figures show the Federal Reserve has engaged in some $16 trillion-worth of transactions, one-third of which were with banks overseas.

As Dr. Paul points out, there's no doubt that foreign banks have been major recipients of Federal Reserve funds.

"We want to know the details of what the agreements were," Paul says, "and whether any of that money will be recouped."

He also points out that an audit could reveal information that no one ever dreamed of, that the Federal Reserve never thought they'd be forced to reveal.

Why Everyone Needs to Educate Themselves about the Federal ReservePeople in general have been largely ignorant of how the Federal Reserve and our monetary- and economic system works, which has given them more or less free reign to run the show any which way they pleased. Fortunately, people are starting to catch on as the financial collapse brought the issue front and center.

At that time, many began to investigate and educate themselves further to understand what was happening.

Still, the conventional media have virtually ignored many of these issues, particularly the issue of international banks being on the receiving end of trillions of dollars of bailout money, which Public Record has dubbed "the biggest scam in world history."

Why is this?

According to Dr. Paul, part of the problem is that the media simply do not understand the issues involved. But the media is also a tightly interwoven part of the management of the United States, and sometimes they simply do not want you to know exactly what's going on.

However, "we do need to give media some credit," Dr. Paul says, stating that both Bloomberg and FOX filed lawsuits under the Freedom of Information Act to get information about where the bailout money went.

Hopefully, if we all rally together and do our part, Congressman Paul's legislation will come to pass and a much needed audit of the Federal Reserve will be done. It will require a coordinated effort by as many people as possible however, as the Federal Reserve will fight tooth and nail to stop it.

Sovereignty is Key

Ron Paul does not worry about how we might abolish the Federal Reserve.

"It will self-destruct," he says.Rather, he worries that they'll simply "patch" the old system with an international currency that we would have even less control over.

So, what's the answer?

"I think the only thing that can protect our sovereignty and sound currency is to make sure enough people know and understand the issue, and demand that we once again become a sovereign nation," he says.

Ron Paul has Introduced Legislation to Opt Out of Government-Run Health Care Plan

Another important piece of legislation introduced by Dr. Paul is a bill that would allow you to opt out of the government-run health care plan without facing stiff fines for refusing to purchase health insurance.

"That way, no matter how bad our system gets, if we have a chance to opt out, it at least gives us some hope," he says. "Hopefully we can just remove the mandate..."He also suggests expanding medical savings accounts, and offering tax breaks for medical spending. I believe he's right when he says that allowing people to take care of their own health without resorting to government-run options only will reduce the burden on the system.

"If we don't, the system will collapse," he says. "No one will have reasonable health care. Costs will go up, doctors will quit, and medical quality will go down."He believes that an opt-out option "might be something President Obama may be forced to accept."

I hope so. There are still serious questions about whether or not mandating the purchase of health insurance is even constitutional.

A federal judge in Florida recently ruled that the individual mandate (the part of the law that forces you to purchase health insurance for yourself and your family) is unconstitutional, CNN reported on January 31. However, other judges have already ruled it constitutional, so the matter will now go to the US Supreme Court.

Should the Supreme Court decide that it violates the constitution, then it may have to be repealed. If they don't, then Dr. Paul's legislation would be of vital importance to provide you an option.

How YOU Can Be Part of the Solution!In this interview, Dr. Paul reaffirms that numbers do matter when it comes to pressuring elected officials into action. Once a politician becomes convinced that it's in their political interest to do something, they will act. So the key is coordinated and organized communication efforts with your Congressmen and other elected officials.

As Dr. Paul says, "they like their jobs." And if they're suddenly bombarded, not by tens but by thousands of their constituents, then the political reality is they're forced to make a choice between keeping their post or satisfying lobbyists. If their voters are silent, then it's easy to be swayed by lobbying groups. But if their jobs are on the line, it's a different story.

I realize very few people take any pleasure whatsoever in getting politically active and involved, but it's quite clear that politicians and large corporate interests have run amok for too long without sufficient feedback and involvement from the people. It's time to re-engage and pay attention to what your elected officials are doing.

Dr. Paul suggests that health groups start to work together in a coordinated fashion with a clear goal in mind, such as supporting a particular piece of legislation.

If you're feeling motivated you can even start a grassroots campaign on your own. The key is to get large numbers of people, to bring a loud and clear message to your elected officials. Last year I posted a helpful ten-point guide to organizing at the grassroots level, created by the director of Californians for Green Dentistry, Anita Vazquez Tibau. These tips are useful for any type of grassroots organization, so here they are again.

Behind the Real Size of the Bailout

A guide to the abbreviations, acronyms, and obscure programs that make up the $14 trillion federal bailout of Wall StreetMother Jones

December 9, 2009

The price tag for the Wall Street bailout is often put at $700 billion—the size of the Troubled Assets Relief Program. But TARP is just the best known program in an array of more than 30 overseen by Treasury Department and Federal Reserve that have paid out or put aside money to bail out financial firms and inject money into the markets. To get a sense of the size of the real $14 trillion bailout, see our chart here. Below, a guide to the pieces of the puzzle:

Treasury Department bailout programs

Money Market Mutual Fund: In September 2008, the Treasury announced that it would insure the holdings of publicly offered money market mutual funds. According to the Special Inspector General for the Troubled Asset Relief Program (SIGTARP), these guarantees could have potentially cost the federal government more than $3 trillion [PDF].

Public-Private Investment Fund: This joint Treasury-Federal Reserve program bought toxic assets from banks and brokerages—as much as $5 billion of assets per firm. According to SIGTARP, the government's potential exposure from the PPIF is between $500 million and $1 trillion [PDF].

TARP: As part of the Troubled Asset Relief Program, the Treasury has made loans to or investments more than 750 banks and financial institutions. $650 billion has been paid out (not including HAMP; see below). As of December 21, 2009, $117.5 billion of that has been repaid.

Government-sponsored enterprise (GSE) stock purchase: The Treasury has bought $200 million in preferred stock from Fannie Mae and another $200 million from Freddie Mac [PDF] to show that they "will remain viable entities critical to the functioning of the housing and mortgage markets."

GSE mortgage-backed securities purchase: Under the Housing and Economic Recovery Act of 2008, the Treasury may buy mortgage-backed securities from Fannie Mae and Freddie Mac. According to SIGTARP, these purchases could cost as much as $314 billion [PDF].

Citigroup asset guarantee: In this joint Treasury, Federal Reserve, and FDIC program, the government agreed to cover potential losses to a Citigroup asset pool worth $301 billion [PDF].

T-bill auctions to fund the Fed: In November 2008, the Treasury announced that it would borrow $260 billion to fund the Supplementary Financing Program, whose proceeds were deposited with the Federal Reserve.

TARP overpayment: This June, the Congressional Budget Office estimated that the federal government would lose $159 billion from its TARP loans and investments due to changes in their market value. (So far, Treasury has earned $14.4 billion in dividends from TARP.)

Bank of America asset guarantee: In this joint Treasury, Federal Reserve, and FDIC program, the government agreed to cover potential losses to a Bank of America asset pool worth $118 billion. Bank of America has withdrawn from the program and has paid the government $425 million [PDF] in compensation.

Potential international fund liabilities: In April, the United States committed up to $100 billion to fund the International Monetary Fund's lending and ensure that it "has adequate resources to play its central role in resolving and preventing the spread of international economic and financial crises."

HAMP: The Home Affordable Modification Program offers financial incentives to lenders to modify home loans. $75 billion in federal funds has been committed; $50 billion of that comes from TARP is set aside to modify mortgages not owned or guaranteed by Frannie Mae, Freddie Mac or other government-sponsored entities.

Treasury exchange stabilization fund: A temporary program to insure the holdings of publicly offered money market mutual funds.

GSE credit facility program: Additional credit made available to Fannie Mae and Freddie Mac. Expires December 31, 2009.

Federal Reserve bailout programs

Commercial Paper Funding Facility: With the support from the Treasury, the Fed established the CPFF in October 2008 to increase the availability of short-term debt (commercial paper) funding. Up to $1.8 trillion [PDF] was earmarked for the program.

Mortgage-backed securities purchase: In 2009, the Fed earmarked up to $1.25 trillion to buy investments based on home loans.

Term Asset-Backed Securities Loan Facility: TALF provides financing to investors who are buying asset-backed securities. In February 2009, the Fed and Treasury announced an expansion of the program to generate up to $1 trillion in new lending.

Foreign Central Bank Currency Liquidity Swaps: The Fed has provided $755 billion [PDF] for currency liquidity swaps with foreign central banks.

Money Market Investor Funding Facility: The MMIF was established in October 2008 to provide loans for investors buying certificates of deposit and commercial paper. According to SIGTARP, $600 billion [PDF] was allocated for the program.

Treasury Purchase Program: In March 2009, the Fed was authorized to purchase up to $300 billion of treasury securities.

GSE Program: In March 2009, the Fed increased its purchases of debt from government-sponsored enterprises (Fannie Mae and Freddy Mac) from $100 billion to $200 billion.

Primary Dealer Credit Facility: The PDCF provides overnight loans to primary dealers (financial firms that can engage in direct transactions with the federal government). The Fed allocated $147.7 billion [PDF] for it in 2009.

ABCP MMMF liquidity facility: The Asset-Backed Commercial Paper (ABCP) Money Market Mutual Fund (MMMF) Liquidity Facility (whew!) provides loans to financial institutions purchasing commercial paper from money market mutual funds. According to SIGTARP, the Fed allocated $145.9 billion for the program in 2009.

JPMorgan Chase/Lehman Brothers: In September 2008, the Fed gave JPMorgan Chase $148 billion in help the near-bankrupt Lehman Brothers.

Open Market Operations: In September 2008, the Fed injected $125 billion into the market by purchasing securities and repurchase agreements, or repos, in which primary dealers borrow cash from the fed.

Tri-Party Repurchase Agreements: The Fed provided $124.6 billion [PDF] for this type of repo in 2009.

Primary Credit: The Fed provided $112 billion [PDF] to offer loans at a discounted rate to eligible institutions in 2009.

Temporary Reserves: Between August and September 2007, the Fed made $93 billion of temporary reserves available for loans to financial firms.

Single-Tranche Repurchase Agreements: In 2009, the Fed offered a total of $80 billion for short-term loans to holders of mortgage-backed securities.

Term Auction Facility: Under TAF, the Fed auctions short-term loans to financial institutions. The amount of loans offered has varied widely; between December 2009 and January 2010, $75 billion in loans will be available.

AIG preferred stock interests, credit, and loan: The Fed provided $53 billion to the struggling AIG in various forms between 2008 and 2009.

AIG Securities Lending Facility: In October 2008, the Fed authorized the Federal Reserve Bank of New York to borrow up to $37.8 billion in securities from AIG.

Maiden Lane II and III (AIG): In 2008, the Fed authorized its New York branch to form three limited liability companies: Maiden Lane, Maiden Lane II, and Maiden Lane III. It provided $52.5 billion to Maiden Lane II and III to assist AIG.

Maiden Lane I (Bear Stearns): The Fed provided $29.8 billion to Maiden Lane I to acquire Bear Stearns' assets and facilitate its merger with JPMorgan Chase.

TSLF: The Term Securities Lending Facility offers Treasury collateral to the Federal Reserve Bank of New York so it can auction weekly loans to financial institutions. $25 billion in loans will be available between November 2009 and January 2010.

TOP: The Term Securities Lending Facility Options Program allowed primary dealers to get TSLF loans in exchange for collateral. At the time of the program's termination in June 2009, $50 billion in loans had been offered.

Expansion of system open market account securities lending: In July 2009, the Fed increased its limit for loans of securities to brokers from $3 billion to $5 billion, for a total of $36 billion [PDF] in new lending.

JPMC/Bear Stearns Loan: The Fed provided a $12.9 billion bridge loan [PDF] to JPMorgan Chase during its acquisition of Bear Stearns.

True Cost of Bailouts: $14 Trillion

NYC MagazineDecember 24, 2009

Although the cost of the Wall Street bailout is usually said to be around $700 billion, the real cost of economic recovery is at least 20 times larger, according to a recent breakdown of ALL of the government recovery programs by Mother Jones Magazine.

The $700 billion bailout that people usually allude to is only the cost of the TARP program that was passed in late 2008 and, even then, the bill that contained the $700 billion for TARP cost $850 billion because of all of the earmarks inside the bill.

Here’s a look at other programs that will ultimately result in $14 trillion in bailouts for Wall Street:

The Money Market Mutual Fund which began in September of 2008 is a program in which the government would “insure the holdings of publicly offered money market mutual funds” and will cost up to $3 trillion.

The Public-Private Investment Fund is a government program that buys up to $5 billion worth of bad assets from big corporations. Ultimately, this is projected to cost anywhere between $500 billion and $1 trillion.

The Fannie Mae and Freddie Mac stock that the government bought alone cost the taxpayer $400 million. The mortgage backed securities that the government bought from Fannie Mae and Freddie Mac will ultimately cost up to $300 billion.

The asset guarantee that the government made to Citibank will cost us around $300 billion.

Other huge costing programs include the asset guarantee that the government made to Bank of America ($118 billion), HAMP, the Treasury exchange stabilization fund, and several Federal Reserve programs which total as much as $7 trillion, making the total bill that the taxpayer has to foot a whopping $14 trillion.

And we were worried that the $700 billion bailout was financially irresponsible…

Fed Handed Out $3.3 Trillion in Crony Deals

Above Top SecretDecember 2, 2010

Half of the criminal fed’s actions have been brought to light.

3.3 trillion taxpayer dollars were handed out in crony deals to banks and other industries.

All the start-ups that stood to benefit from the collapse of the behemoths were denied justice in the market by the criminal actions of a handful of men.

The WaPo reports:

The banks universally hailed the Fed on Wednesday.

“In late 2008, many of the US funding markets were clearly broken,” Goldman Sachs said in a statement, echoing similar comments made by Bank of America and Citigroup. “The Federal Reserve took essential steps to fix these markets and its actions were very successful.”By 2009, Goldman and other Wall Street firms were reporting their best profits ever. That allowed these banks to pay out huge salaries again, but it also drew the ire of lawmakers and ordinary Americans.

Of course they universally hailed the Fed.

Without the Fed, they would all be bankrupt.

The entire purpose of the Fed is to prevent the mega commercial banks from going out of business.

One man made the call to allocate nearly a quarter of the entire American GDP to all manner of crony corporations and criminal banking institutions.

Democracy? LOL

And of course, this $3.3 trillion does not include the bailouts of Fannie and Freddie, nor does it include all the money allocated by congress. Those bailouts are in the tens of trillions.

Basically every major corporation in America got money taken from the pockets of the tax payer in some manner. Either through direct bailouts by the Fed, handouts from congress, or crony government deals.

The message to industry is as follows:

Washington pays.

Ford, BMW, Toyota Took Secret Government Money

JalopnikDecember 4, 2010

In the depths of the financial collapse, the U.S. Federal Reserve pumped $3.3 trillion into keeping credit moving through the economy. It eventually lent $57.9 billion to the auto industry — including $26.8 billion to Ford, Toyota and BMW.

The Fed on Wednesday was forced to reveal the identity of the companies it aided during the crisis, after contending to Congress that keeping their identities and the details of such lending secret was essential. Much of Wall Street, and corporate giants such as General Electric, Harley Davidson and McDonald's, took advantage of the Fed's help. We've done the math on how the Fed propped up the auto industry.

While Chrysler and General Motors had to go to Congress to beg for cash in 2008, every other automaker's finance arm was having trouble as well. Typically, once they lend money to a buyer, they sell the loan, get the cash upfront, then pump the proceeds back into the business. They also take out short-term loans called commercial paper that keeps the day-to-day business afloat. The crash cut the circuit, raising the chances the automakers couldn't make loans to buyers and keep selling new vehicles.

That's where the Fed stepped in. In normal circumstances, the Fed only lends money to banks, leaving the decisions about who should get credit to them. But when the financial markets started to collapse in late 2008, the Fed set up several programs to lend money directly to corporations, a highly unusual step.

According to the data, from October 2008 through June 2009 the fed bought $45.1 billion in commercial paper from the credit arms of four automakers - Ford, BMW, Chrysler and Toyota - along with GMAC (the former General Motors credit arm). Of those, Ford sold the most, with $15.9 billion.

The Fed also lent $13 billion to investors who bought bonds backed by loans to new car buyers from automakers and banks. The Fed made clear that while investors got the loans, the move was meant to keep the lenders in business; the credit arms of Ford, Chrysler, Nissan, Volkswagen, Honda and Hyundai all benefited directly.

Ford spokeswoman Christin Baker said the two programs "addressed systemic failure in the credit markets, and that neither program was designed for a particular company, or even a particular industry." Ford Credit has disclosed through SEC filings and conference calls with media and investors that it was taking part in both programs.

BMW told Bloomberg that the Fed lending "supported our financial profile and offered us an additional funding source, especially at times when the money markets and capital markets did not function properly and efficiently."

According to the Fed, the commercial paper loans have been paid in full, while some $2 billion remains outstanding on loans for bond investors.

The secrecy surrounding the details of the loans only masked how much aid corporate America and Wall Street needed. While General Motors and Chrysler took the brunt of the blowback for relying on government handouts, the reveal of the Fed numbers show that a far bigger slice of the U.S. auto industry needed help.

No comments:

Post a Comment